How the SECURE Act Messed Up Inheriting IRAs | Tax Planning

A lot of our clients now understand this, but the IRS slipped in a new rule with the passing of SECURE Act in 2020 that would allow them to collect taxes on pre-tax IRAs faster when someone passes away. Prior to the SECURE act passing, most non-spouse beneficiaries could use their life expectancy to distribute funds from an IRA – a strategy called the “stretch IRA”. The SECURE act now requires most non-spouse beneficiaries more than 10 years younger than the account owner that died to take deplete the account within 10 years.

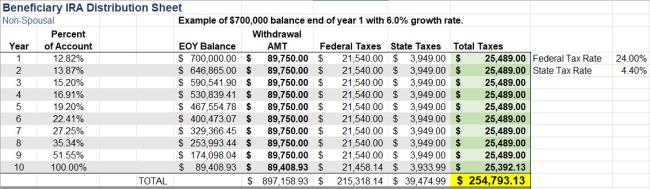

What does this REALLY mean? If you pass a pre-tax IRA (Traditional, SEP, etc.) to your children they will have 10 years to pay the taxes owed on those funds. If you live to your life expectancy – mid-80’s for most of us – your children will likely be in THEIR highest income earning years. Let’s use some hypothetical numbers to illustrate the impact.

*This is a hypothetical example and is not representative of any specific investment. Your results may vary.

As you can see above, in order to evenly distribute the funds that are growing at a steady 6% rate, the beneficiary would have to take approximately $89,000 per year and add it to their income to satisfy the requirements of the IRS. The tax bill over the 10-year period is just over $250,000 at 24% Federal and 4.4% State (CO) tax rates!

The workaround here is to GET AHEAD of your tax bill. You can work with your tax preparer and financial professionals to start paying that tax bill now and convert that pre-tax bucket to a tax-free bucket. Your non spouse beneficiaries will NOT have the option to convert these assets to a tax-free bucket like you do now. Roth IRA still has the same 10-year requirements imposed by the SECURE act, but those funds can come out TAX-FREE.

Last thing: The IRS is NOT currently requiring beneficiaries to take those amounts out of inherited accounts. They are allowing the tax bill to get kicked down the road while the growth on these accounts will still owe taxes. We work with our clients that have (non-spousal) inherited pre-tax IRAs to strategically get the funds out of these accounts now even though the IRS does not require it. The sheet above is something that we designed to help guide us as we make annual adjustments based on investment performance, tax return reviews, and life changes.

Next up: Why Reviewing Your Withholding is Important

Disclosures

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

A Roth IRA offers tax deferral on any earnings in the account. Qualified withdrawals of earnings from the account are tax-free. Withdrawals of earnings prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Limitations and restrictions may apply.